The 2018 IHRSA Profiles of Success facilitates strong, steady performance by clubs.

It’s become an important and much-anticipated tradition—the release of the findings from IHRSA’s annual Industry Data Survey (IDS) and the resulting publication, IHRSA Profiles of Success.

In October, the association published the 36th annual edition of ‘Profiles’, the exhaustive and authoritative report that many clubs use to benchmark their operations, comparing their performance with that of their peers to identify their strengths, weaknesses, and opportunities for improvement.

“Highly successful organisations understand the importance of benchmarking and the value of measuring key performance metrics against those of comparable businesses,” observes Brent Darden, a principal at Brent Darden Consulting, in Dallas, Texas, and past chairperson of IHRSA’s board of directors. “As the saying goes, ‘what gets measured gets managed,’ and Profiles of Success offers a credible foundation for reinforcing this management habit.”

“Highly successful organisations understand the importance of benchmarking and the value of measuring key performance metrics against those of comparable businesses,” observes Brent Darden, a principal at Brent Darden Consulting, in Dallas, Texas, and past chairperson of IHRSA’s board of directors. “As the saying goes, ‘what gets measured gets managed,’ and Profiles of Success offers a credible foundation for reinforcing this management habit.”

The former owner and general manager of the TELOS Fitness Centre, in Dallas, Darden recalls, “At my club, it provided a useful platform for learning and growth.”

In total, 112 club companies, 12,289 fitness facilities, contributed their time and effort to complete the 2018 survey, which addressed their 2017 performance.

“This 76-page report provides detailed analysis of the accomplishments of leading IHRSA member clubs, providing key metrics on income, payroll, other expenses, non-dues revenue, membership growth, club traffic, retention, and EBITDA (earnings before interest, taxes and amortisation),” explains Melissa Rodriguez, IHRSA’s senior research manager. “Club operators can use it to compare their performance across profit centres and a wide range of other categories.”

“Along with The IHRSA Health Club Consumer Report, Profiles is a must have resource for any operator who wants to better understand how well their club is doing, what consumers want, and, ultimately, how to grow their business.”

Positive Indicators

In general, how did clubs fare in 2018?

“Results from the IDS indicate that leading operators have continued to grow revenue and membership at healthy rates,” reports Jay Ablondi, IHRSA’s executive vice president of global products. “Clubs posted strong financial and membership numbers, with results varying by club type and size.”

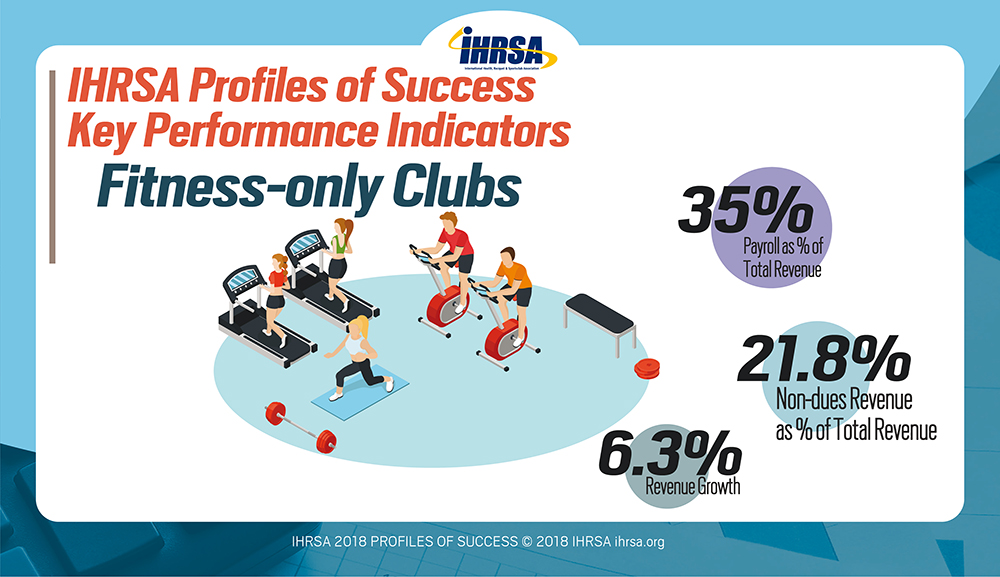

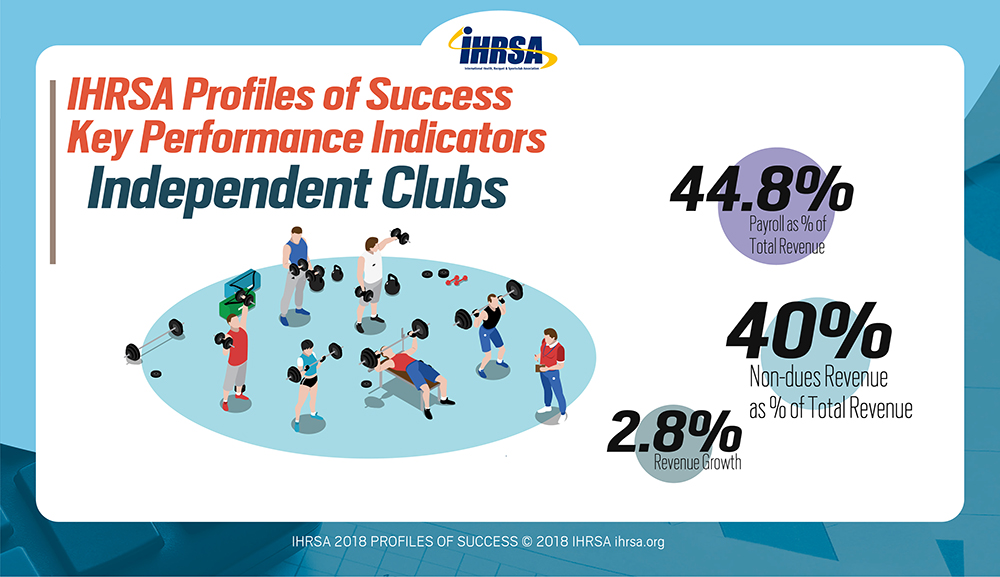

Overall, the respondents reported increases of 5.3% and 2.8% in revenue and membership, respectively. Clubs that are part of a chain reported higher revenue growth (+7%) than independent ones (+2.8%). Conversely, independents, with a retention rate of 72.4%, outperformed chain operations, at 66.7%. In terms of club size, larger facilities generated significantly more revenue per member per year (US$975.30 – AU$1383) than smaller ones (US$479.70 – AU$680.21).

Overall, the respondents reported increases of 5.3% and 2.8% in revenue and membership, respectively. Clubs that are part of a chain reported higher revenue growth (+7%) than independent ones (+2.8%). Conversely, independents, with a retention rate of 72.4%, outperformed chain operations, at 66.7%. In terms of club size, larger facilities generated significantly more revenue per member per year (US$975.30 – AU$1383) than smaller ones (US$479.70 – AU$680.21).

The respondents also reported that, in 2017, US$3 ($AU4.25) out of every US$10 (AS$14.18) of income came from non-dues related services, i.e., personal training, Pilates, nutritional counselling, spa services, and other offerings. “That’s a valuable statistic because, historically, non-dues revenues has not only contributed to the bottom line, but also has been linked to higher retention,” Rodriguez points out. “The industry axiom, ‘The more they pay, the longer they stay,’ remains valid.”

The fact that the clubs encompassed by the study continue to hold onto seven out of 10 of their members testifies to their success in creating a strong, symbiotic relationship with them, she stresses.

High retention is critical in that it allows clubs to spend less money and staff time on recruiting new members.

It’s important to note that, while the sales and marketing costs associated with new accounts had been declining for three consecutive years—from a high of US$118 (AU$167.32) in 2013, to a low of US$66 (AU$93.59) in 2016—that figure jumped to US$98 (AU$138.96) in 2017. It’s a clear indication that the competition for new members has been heating up.

Fees and Dues

What about prices? In the past, they’ve tended to vary greatly, and 2017 was no exception.

As a club’s total indoor square footage increases, prices increase as well, which is reasonable, since facilities with more space can offer more activities, services, and amenities, which consumers are willing to pay for.

Predictably, multipurpose clubs reported that they were able to assess significantly higher initiation fees and monthly dues 66% greater than those changed by fitness-only facilities.

The median figure for all clubs was US$74 (AU$104.93) for enrolment fees and US$61 (AU$86.50) for monthly dues. The US$74 (AU$104.93) enrolment represents an increase of nearly 14% over the US$65 (AU$92.17) charged in 2016. Over the course of a year, club members paid a median of US$732 (AU$1037.98) in annual dues, an increase over the US$720 (AU$1020.96) reported in 2016.

Such increases could be an indication that, given a stronger economy in 2017, some consumers may be becoming a little less price sensitive.

Also, 16% of the respondents indicated that they levied no enrolment or initiation fee, a slight drop from 17% in 2016, and well below the 23% reported in 2014.

“Such variations in price might be difficult for consumers to reconcile,” Rodriguez concedes. “However, the variety of pricing options ensures that each consumer is able to find the price point that’s right for them.

However, the issue of pricing will continue to be very important going forward, as concerns about inflation and interest rate hikes weigh on both clubs and consumers.”

Staffing and Payroll

Labour is always a substantial expense for clubs, one that operators follow closely and attempt to control, and, in 2017, the survey respondents were largely successful in doing so. Staff levels and expenses remained relatively flat.

For the most part, employee levels have stabilised since many clubs “right-sized” in 2009, following the severe economic slump of 2008, In 2010, some began hiring when the economy began to improve, but others discovered that they were able to “do more with less” without compromising member service. That seems to remain a viable strategy.

Today, according to Profiles, the typical club employs about 13 full-time and 45 part-time staff. Employee head counts were relatively stable for most types of facilities. Many clubs employ part-timers to ramp up, or down, as needed, and, balancing the scales, when the number of part-timers falls, the number of full-timers tends to rise.

Similarly, payroll as a percent of revenue was nearly constant, at 43.4% in 2017 vs. 43.7% in 2016. Each full-time equivalent employee generated an average of US$97,810 (AU$138,964) for their employer for the year.

Obtaining the IHRSA Profiles of Success Report

The 2018 IHRSA Profiles of Success is the most accurate and up-to-date industry benchmarking resource available. To purchase the complete report, log on to ihrsa.org/profiles or call +1 617-951-0055. The cost is for the Profiles of Success Report is AU$249.95 for IHRSA members and AU$499.95 for non-members.

Founded in 1981, IHRSA – International Health, Racquet & Sportsclub Association – is the industry’s global trade association, representing more than 10,000 health and fitness facilities and suppliers worldwide. To learn how IHRSA can help your business thrive, visit www.ihrsa.org. John Holsinger, IHRSA’s Director, Asia Pacific, can be contacted at jwh@ihrsa.org or on mobile 0437 393 369.[/box]

This article was written for the What’s New in Fitness Magazine Summer 2018 Edition by Kristen Walsh, Associate Publisher for IHRSA and regular columnist for Club International. You can contact Kristen through the main www.ihrsa.org website. To view other related articles written b Kristen – click here.

This article was written for the What’s New in Fitness Magazine Summer 2018 Edition by Kristen Walsh, Associate Publisher for IHRSA and regular columnist for Club International. You can contact Kristen through the main www.ihrsa.org website. To view other related articles written b Kristen – click here.